There comes a time in everyone’s life when they must make a choice about when to begin taking their Social Security benefits. The conventional wisdom shared by many investment advisers is that the longer you wait, the better. You can choose to begin taking benefits anytime between the ages of 62 and 70. The catch here is that each year after age 62 that you delay taking benefits means an increase in the monthly amount up to the age of 70 after which there is no benefit to any further delays.

There are many Social Security calculators out there but most do not consider important factors such as inflation, the Cost Of Living Allowance (COLA) which is the number the government comes up with every year to determine the annual increase in Social Security benefits, the return on your investments, taxes, etc. The main reason these calculators ignore these important inputs is that predicting rates over long periods of time isn’t an exact science.

But I don’t think that ignoring them altogether is the correct approach either. We know that rates are not going to be zero (except perhaps for the current rate of return on conservative fixed income investments such as Treasuries) and any reasonable assumption will produce more realistic results than omitting them altogether. In an attempt to assess the differences, I wrote my own calculator taking into consideration the above mentioned factors. This article will show how the addition of these factors can make a big difference in determining the optimum time to begin taking benefits and we’ll see that the optimum time is not always in alignment with the conventional wisdom.

The calculator

The figure below shows the data fields that form the inputs to the calculations. Note that this calculator does not consider the complex issue of spousal benefits or benefit penalties for continuing to work while receiving benefits. This latter issue is discussed at the end of this article.

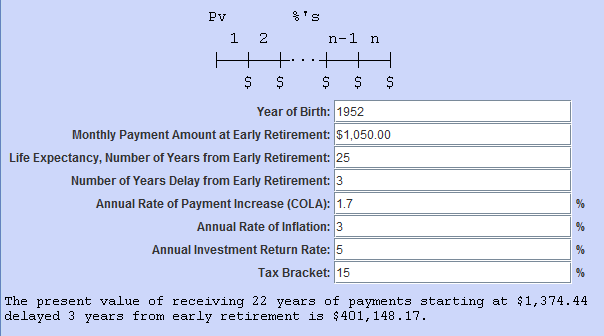

Figure 1. Calculator Parameters

Present Value vs Total Payments

The crux of the computation is the net Present Value (PV), the stream of payments made to you discounted back to today’s dollars. [The net Present Value is illustrated at the top of Figure 1 where the Present Value (Pv) is today and payments are received monthly starting one month from today.] This is the main difference between the approach here and the usual approach which is to consider only unadjusted absolute amounts. That is, the total amount of benefits you will have received at the end of your life based on your life expectancy.

The factors mentioned above, inflation, COLA, investment return, and taxes along with the benefit increase you would get by delaying taking benefits, are all included in the calculator’s analysis. The latter values can be found in this table on the Social Security web site. Using these and your personal information (more about these in a minute), the calculator figures out the optimum number of years you should delay benefits based on the maximum total dollar value of your benefits package. This sum is expressed in today’s dollars. [Note that the rate of benefit increases due to delay in taking them are based on your year of birth.]

Determination of your personal input parameters

Besides your year of birth, the parameters you will need to input are the “Monthly Payment Amount at Early Retirement” and your estimated life expectancy.

The monthly payment amount can be obtained from your personal benefits calculator on the Social Security Website. This number is your monthly check amount if you begin taking benefits at age 62. It is based on your earnings history and you must provide secure personal information to obtain it. Let’s assume for this analysis that you were born in 1952 (you are now 61) and your monthly benefit will start at $1,050 per month. This may or may not be a typical amount.

The “Life Expectancy” field is the number of years you expect to live beyond age 62. Here is an average life expectancy calculator from the Social Security website. If you want more precise probabilities, there is a calculator on the Vanguard web site. Using the Vanguard calculator, Figure 2 is a plot of the probability of reaching a certain age for the average 62 year old American.

Figure 2. Life Expectancy

An Example

Let’s input some typical values and see what the calculator tells us. Let’s assume that you are now 62 and expect to enjoy life for another 25 years. Judging by Figure 2, your estimate may be a bit optimistic as the likelihood of living to 87 is 44% if you’re female and only 31% if you’re male. (On the glass half-full side, health care could improve in the near future which would up these percentages.)

The current COLA is 1.7% per the U.S. Government experts on how your cost of living is increasing each year. That may have nothing at all to do with reality. The annual rate of inflation is how fast costs are really increasing and are expected to increase in the near future. Let’s assume a value of 3% over the long haul. [FYI, retirement homes are currently adjusting their rent and annual service increases by 5% per year.]

The investment return rate should be based on a fairly conservative portfolio because you need the money now and can’t afford to sit out prolonged bear markets in volatile investments. Let’s say your portfolio will return on average 5% annually over the next 25 years.

If you will be spending your benefit check each month rather than adding it to your portfolio then enter zero for the investment return rate. This can alter the results substantially. Your tax bracket should also be low as you are no longer working and generating wage income. Let’s assume 15% and pray there are no increases in the tax rate.

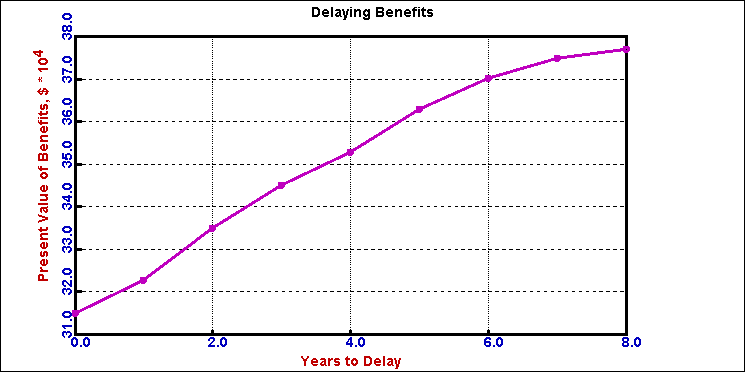

Based on these inputs, you should wait three years until the age of 65 to begin taking benefits. The Present Value of the stream of benefit payments over 22 (25 minus 3) years will be just over $400,000. You can try other “Number of Years Delay” from 0 to 8 and see how these compare. The calculator actually does this automatically and plots the results. For this example, the plot is shown in Figure 3 below.

Figure 3. Delaying Benefits Considering Various Percentage Rates

You can see that by delaying taking benefits until the age of 65 produces the highest net Present Value of the stream of payments. It is not a simple increase where the longer you delay the better. In this example, taking benefits anywhere between two and four years won’t make a huge difference, but delaying benefits for more than five years can make a significant dent in your overall retirement income.

The impact of life expectancy

Another analysis you can do with the calculator is to vary your life expectancy. Using the input values in the above example and varying the life expectancy up to 40 years, the graph in Figure 4 is generated. Each data point in this plot represents the optimum number of years to delay from an associated plot similar to Figure 3 above.

Figure 4. Life Expectancy Analysis Considering Various Percentage Rates

Figure 4 is very interesting in that it tells you that you’ll be better off taking benefits right away if you expect to live for up to 23 more years. After that, the best delay rises until it maxes out at age 70 which won’t be optimal until you reach the near-centenarian age of 98, not very likely for either sex according to Figure 2.

The effect of varying the rate of return on investments

Varying the assumed investment rate of return affects the Present Value of your total benefits considerably as well as the optimum number of years to delay. Table 1 below shows these results based on the example above.

| Rate | Present Value | Best Years Delay |

|---|---|---|

| 0% | $260,003 | 7 |

| 1% | $281,239 | 7 |

| 2% | $305,405 | 6 |

| 3% | $332,566 | 6 |

| 4% | $363,901 | 5 |

| 5% | $401,148 | 3 |

| 6% | $447,236 | 0 |

| 7% | $504,336 | 0 |

| 8% | $570,304 | 0 |

| 9% | $646,685 | 0 |

| 10% | $735,309 | 0 |

To summarize, the lower the return on your investments, the longer you should wait until taking benefits.

Other considerations

You can see how important it is to consider the litany of variables that pertain to this question of when to best start taking your Social Security benefits. If you construct a table similar to the one above that varies the rate of inflation, the results will be that the greater the disparity between the actual rate of inflation over the COLA, the more important it is to take benefits now and not delay. Raising your tax bracket does not affect the number of years to best delay; it merely lowers your expected return in current dollars.

Results if You Don’t Discount

The reason this article was written in the first place was to see if the common assumption of ignoring factors such as inflation, COLA, investment return, and taxes was the right thing to do. In that regard, let’s zero those out and perform the computations again. Using the input parameters and assumptions in the example, Figure 5 shows the value of taking benefits for the various years of delay. You can see that, in this instance, it is apparently better to delay taking benefits as long as possible.

Figure 5. Delaying Benefits Without Discounting

Life Expectancy Analysis Without Discounting

Figure 6 below repeats Figure 4 but uses percentage rates of zero on COLA, inflation, and investment return, and taxes. In this case, delaying benefits is beneficial if you live for a mere 14 additional years. According to Figure 2, this represents a 75% chance for a man and an 80% chance for a woman. If you expect to live after the age of 85 (roughly the current life expectancy), then you’ll receive no extra benefit for waiting. Funny how that worked out!

Figure 6. Life Expectancy Analysis Without Discounting

Further thoughts and the future of Social Security

Based on these last two charts, it would seem that delaying benefits as long as possible is the best way to go. Unfortunately, this is what drives conventional wisdom. Ignoring important interest rate factors, as we have seen, can make a huge difference.

So far we have examined this problem from a purely theoretical point of view. All well and good but these analyses won’t amount to that proverbial hill of beans unless the government cooperates.

What the analysis here does not take into account are the fundamental risks: the risk of government action to reduce or potentially even eliminate your benefits based on some arbitrary criteria in the future to meet some perceived financial crisis. Benefit reductions, COLA elimination, means testing, retirement age increases, changes in the tax code, etc. These are all potential threats that could severely affect your monthly benefit check. Social Security, after all, is not a welfare program; it is your money that you already paid to the government that is being given back to you. The problem is that this money has been spent, not saved, by the government who is passing the buck to the younger generation. But the problem is that the worker base (i.e., young people entering the work force) is eroding which could spell real trouble for the certainty of your benefits in the future.

As explained in this publication the Social Security administration really wants you to be actually retired before you take your benefits. If you need to keep working beyond age 62 up to your full retirement age they will penalize you by reducing your benefits by $1 for every $2 you earn over the current wage limit, currently $15,120. So, if you earn substantially more than this through wages, that could wipe out all of your benefits. In this case it would make no sense to take your benefits until you truly stop working or reduce your earned income substantially.

Try the calculator yourself

You can try this calculator yourself by running the demo of the Portfolio Preserver asset allocation software. Bring up the Java program demo from the “Preserver Professional” page, Select “Calculations” from the menu bar at the top of the screen, then select “Financial Calculations” from the pull down menu, and then select the “Social Security Payout” tab. [Note: You will probably need the latest version of Java available here. Also, the software is not always compatible with Apple devices.]

As with all such exercises, readers are advised to consult their own investment professional or accountant before making any decisions regarding their personal finances.